PRODUCER-CONSUMER

In this simple example program, Producer-Consumer Pattern has been used. CopulaQueue class is nothing more, than just a wrapper for thread-safe ConcurrentQueue data structure. More specifically, the part of the program which actually creates all correlated random numbers into CopulaQueue, is the Producer. In the program, concrete CopulaEngine implementation class takes concrete RandomGenerator implementation class and correlation matrix as its input parameters. Concrete CopulaEngine implementation class then creates correlated random numbers and uses C# Event for sending created random number matrices to CopulaQueue. Another part of the program is the Consumer. Here, I have created a simple consumer class which simply prints created random numbers to console. Consumer class also uses C# Event for Dequeueing random number matrices from CopulaQueue. Needless to say, this (Consumer) is the part of our program, where we should be utilizing all correlated random numbers created by the Producer.

On design side, this program is closely following the program presented in the blog posting referred above. Again, the beef in this design is on its flexibility to allow any new implementations for Random generator and Copula model. Moreover, our example program is using C# Framework Parallel class method Parallel.ForEach, found under System.Threading.Tasks namespace. Example program creates four producers and consumers (both into List data structure) and using multi-threading (Parallel.ForEach) when processing correlated random numbers into/from CopulaQueue.

C# PROGRAM

In order to make everything as smooth as possible for the program replication, I have been writing all required classes in the same file. Just create a new console application and copy-paste the following program into a new .cs file.using System; using System.Diagnostics; using System.Linq; using System.Collections.Generic; using System.Threading.Tasks; using System.Collections.Concurrent; // namespace MultithreadingCopula { // public delegate methods needed for sending and receiving matrix data public delegate void MatrixSender(double[,] matrix); public delegate double[,] MatrixReceiver(); // ******************************************************************** // // the main program class Program { static void Main(string[] args) { try { // start timer Stopwatch timer = new Stopwatch(); timer.Start(); // // PRODUCER PART // create copula implementation, correlation matrix data and list of copula engines CopulaQueue copulaQueue = new CopulaQueue(); double[,] correlationMatrix = createCorrelationMatrix(); List<CopulaEngine> engines = new List<CopulaEngine>(); int nEngines = 4; int nRandomArrays = 25000; for (int i = 0; i < nEngines; i++) { engines.Add(new GaussianCopula(nRandomArrays, correlationMatrix, new CSharpRandom())); ((GaussianCopula)engines[i]).SendMatrix += copulaQueue.Enqueue; } // process all copula engines (producers) in parallel Parallel.ForEach(engines, engine => engine.Process()); // // CONSUMER PART // create list of consumers List<Consumer> consumers = new List<Consumer>(); int nConsumers = nEngines; for (int i = 0; i < nConsumers; i++) { consumers.Add(new Consumer(nRandomArrays, "consumer_" + (i + 1).ToString())); consumers[i].ReceiveMatrix += copulaQueue.Dequeue; } // process all consumers in parallel Parallel.ForEach(consumers, consumer => consumer.Process()); // // stop timer, print elapsed time to console timer.Stop(); Console.WriteLine("{0} {1}", "time elapsed", timer.Elapsed.TotalSeconds.ToString()); } catch (AggregateException e) { Console.WriteLine(e.Message.ToString()); } } // hard-coded data for correlation matrix static double[,] createCorrelationMatrix() { double[,] correlation = new double[5, 5]; correlation[0, 0] = 1.0; correlation[0, 1] = 0.748534249620189; correlation[0, 2] = 0.751; correlation[0, 3] = 0.819807151586399; correlation[0, 4] = 0.296516443152486; correlation[1, 0] = 0.748534249620189; correlation[1, 1] = 1.0; correlation[1, 2] = 0.630062355599386; correlation[1, 3] = 0.715491543000545; correlation[1, 4] = 0.329358787086333; correlation[2, 0] = 0.751; correlation[2, 1] = 0.630062355599386; correlation[2, 2] = 1.0; correlation[2, 3] = 0.758158276137995; correlation[2, 4] = 0.302715778081627; correlation[3, 0] = 0.819807151586399; correlation[3, 1] = 0.715491543000545; correlation[3, 2] = 0.758158276137995; correlation[3, 3] = 1.0; correlation[3, 4] = 0.286336231914179; correlation[4, 0] = 0.296516443152486; correlation[4, 1] = 0.329358787086333; correlation[4, 2] = 0.302715778081627; correlation[4, 3] = 0.286336231914179; correlation[4, 4] = 1.0; return correlation; } } // ******************************************************************** // // consumer class for correlated random numbers public class Consumer { public event MatrixReceiver ReceiveMatrix; public string ID; private int n; // public Consumer(int n, string ID) { this.n = n; this.ID = ID; } public void Process() { for (int i = 0; i < n; i++) { // get correlated 1xM random matrix from CopulaQueue and print it to console double[,] matrix = ReceiveMatrix(); Console.WriteLine("{0} {1} {2} {3} {4} {5}", this.ID, Math.Round(matrix[0, 0], 4), Math.Round(matrix[0, 1], 4), Math.Round(matrix[0, 2], 4), Math.Round(matrix[0, 3], 4), Math.Round(matrix[0, 4], 4)); // } } } // ******************************************************************** // // abstract base class for all uniform random generators public abstract class RandomGenerator { public abstract double GetUniformRandom(); } // ******************************************************************** // // uniform random generator implementation by using CSharp Random class public class CSharpRandom : RandomGenerator { private Random generator; // public CSharpRandom() { // using unique GUID hashcode as a seed generator = new Random(Guid.NewGuid().GetHashCode()); } public override double GetUniformRandom() { // Random.NextDouble method returns a double greater than or equal to 0.0 // and less than 1.0. Built-in checking procedure prevents out-of-bounds random // number to be re-distributed further to CopulaEngine implementation. double rand = 0.0; while (true) { rand = generator.NextDouble(); if (rand > 0.0) break; } return rand; } } // ******************************************************************** // // abstract base class for all specific copula implementations public abstract class CopulaEngine { // Uniform random generator and correlation matrix are hosted in this abstract base class. // Concrete classes are providing algorithm implementation for a specific copula // and event mechanism for sending created correlated random numbers matrix data to CopulaQueue class. protected RandomGenerator generator; protected double[,] correlation; // public CopulaEngine(double[,] correlation, RandomGenerator generator) { this.correlation = correlation; this.generator = generator; } public abstract void Process(); } // ******************************************************************** // // concrete implementation for gaussian copula public class GaussianCopula : CopulaEngine { public event MatrixSender SendMatrix; private double[,] normalRandomMatrix; private double[,] choleskyMatrix; private double[,] correlatedNormalRandomMatrix; private double[,] correlatedUniformRandomMatrix; private int rows; private int cols; // public GaussianCopula(int n, double[,] correlation, RandomGenerator generator) : base(correlation, generator) { this.cols = base.correlation.GetUpperBound(0) + 1; // M, number of variables this.rows = n; // N, number of 1xM matrices } public override void Process() { // NxM matrix containing of uniformly distributed correlated random variables are calculated // as a sequence of specific matrix operations createNormalRandomMatrix(); createCholeskyMatrix(); correlatedNormalRandomMatrix = MatrixTools.Transpose(MatrixTools.Multiplication(choleskyMatrix, MatrixTools.Transpose(normalRandomMatrix))); createCorrelatedUniformRandomMatrix(); } private void createNormalRandomMatrix() { // create NxM matrix consisting of normally distributed independent random variables normalRandomMatrix = new double[rows, cols]; for (int i = 0; i < rows; i++) { for (int j = 0; j < cols; j++) { normalRandomMatrix[i, j] = StatTools.NormSInv(base.generator.GetUniformRandom()); } } } private void createCholeskyMatrix() { // create lower-triangular NxM cholesky decomposition matrix choleskyMatrix = new double[cols, cols]; double s = 0.0; // for (int j = 1; j <= cols; j++) { s = 0.0; for (int k = 1; k <= (j - 1); k++) { s += Math.Pow(choleskyMatrix[j - 1, k - 1], 2.0); } choleskyMatrix[j - 1, j - 1] = base.correlation[j - 1, j - 1] - s; if (choleskyMatrix[j - 1, j - 1] <= 0.0) break; choleskyMatrix[j - 1, j - 1] = Math.Sqrt(choleskyMatrix[j - 1, j - 1]); // for (int i = j + 1; i <= cols; i++) { s = 0.0; for (int k = 1; k <= (j - 1); k++) { s += (choleskyMatrix[i - 1, k - 1] * choleskyMatrix[j - 1, k - 1]); } choleskyMatrix[i - 1, j - 1] = (base.correlation[i - 1, j - 1] - s) / choleskyMatrix[j - 1, j - 1]; } } } private void createCorrelatedUniformRandomMatrix() { // map normally distributed numbers back to uniform plane // process NxM matrix row by row for (int i = 0; i < rows; i++) { // create a new 1xM matrix for each row and perform uniform transformation correlatedUniformRandomMatrix = new double[1, cols]; for (int j = 0; j < cols; j++) { correlatedUniformRandomMatrix[0, j] = StatTools.NormSDist(correlatedNormalRandomMatrix[i, j]); } // event : send transformed 1xM matrix to CopulaQueue this.SendMatrix(correlatedUniformRandomMatrix); } } } // ******************************************************************** // // this is technically just a wrapper class for ConcurrentQueue data structure public class CopulaQueue { private ConcurrentQueue<double[,]> queue; public CopulaQueue() { queue = new ConcurrentQueue<double[,]>(); } public void Enqueue(double[,] matrix) { // insert a matrix into data structure queue.Enqueue(matrix); } public double[,] Dequeue() { // remove a matrix from data structure double[,] matrix = null; bool hasValue = false; while (!hasValue) hasValue = queue.TryDequeue(out matrix); return matrix; } } // ******************************************************************** // // collection of methods for different types of statistical calculations public static class StatTools { // rational approximation for the inverse of standard normal cumulative distribution. // the distribution has a mean of zero and a standard deviation of one. // source : Peter Acklam web page home.online.no/~pjacklam/notes/invnorm/ public static double NormSInv(double x) { const double a1 = -39.6968302866538; const double a2 = 220.946098424521; const double a3 = -275.928510446969; const double a4 = 138.357751867269; const double a5 = -30.6647980661472; const double a6 = 2.50662827745924; // const double b1 = -54.4760987982241; const double b2 = 161.585836858041; const double b3 = -155.698979859887; const double b4 = 66.8013118877197; const double b5 = -13.2806815528857; // const double c1 = -7.78489400243029E-03; const double c2 = -0.322396458041136; const double c3 = -2.40075827716184; const double c4 = -2.54973253934373; const double c5 = 4.37466414146497; const double c6 = 2.93816398269878; // const double d1 = 7.78469570904146E-03; const double d2 = 0.32246712907004; const double d3 = 2.445134137143; const double d4 = 3.75440866190742; // const double p_low = 0.02425; const double p_high = 1.0 - p_low; double q = 0.0; double r = 0.0; double c = 0.0; // if ((x > 0.0) && (x < 1.0)) { if (x < p_low) { // rational approximation for lower region q = Math.Sqrt(-2.0 * Math.Log(x)); c = (((((c1 * q + c2) * q + c3) * q + c4) * q + c5) * q + c6) / ((((d1 * q + d2) * q + d3) * q + d4) * q + 1); } if ((x >= p_low) && (x <= p_high)) { // rational approximation for middle region q = x - 0.5; r = q * q; c = (((((a1 * r + a2) * r + a3) * r + a4) * r + a5) * r + a6) * q / (((((b1 * r + b2) * r + b3) * r + b4) * r + b5) * r + 1); } if (x > p_high) { // rational approximation for upper region q = Math.Sqrt(-2 * Math.Log(1 - x)); c = -(((((c1 * q + c2) * q + c3) * q + c4) * q + c5) * q + c6) / ((((d1 * q + d2) * q + d3) * q + d4) * q + 1); } } else { // throw if given x value is out of bounds (less or equal to 0.0, greater or equal to 1.0) throw new Exception("input parameter out of bounds"); } return c; } public static double NormSDist(double x) { // returns the standard normal cumulative distribution function. // the distribution has a mean of zero and a standard deviation of one. double sign = 1.0; if (x < 0) sign = -1.0; return 0.5 * (1.0 + sign * errorFunction(Math.Abs(x) / Math.Sqrt(2.0))); } private static double errorFunction(double x) { // uses Hohner's method for improved efficiency. const double a1 = 0.254829592; const double a2 = -0.284496736; const double a3 = 1.421413741; const double a4 = -1.453152027; const double a5 = 1.061405429; const double a6 = 0.3275911; x = Math.Abs(x); double t = 1 / (1 + a6 * x); return 1 - ((((((a5 * t + a4) * t) + a3) * t + a2) * t) + a1) * t * Math.Exp(-1 * x * x); } } // ******************************************************************** // // collection of methods for different types of matrix operations public static class MatrixTools { public static double[,] Transpose(double[,] matrix) { // method for transposing matrix double[,] result = new double[matrix.GetUpperBound(1) + 1, matrix.GetUpperBound(0) + 1]; // for (int i = 0; i < matrix.GetUpperBound(0) + 1; i++) { for (int j = 0; j < matrix.GetUpperBound(1) + 1; j++) { result[j, i] = matrix[i, j]; } } return result; } public static double[,] Multiplication(double[,] matrix1, double[,] matrix2) { // method for matrix multiplication double[,] result = new double[matrix1.GetUpperBound(0) + 1, matrix2.GetUpperBound(1) + 1]; double v = 0.0; // for (int i = 0; i < matrix1.GetUpperBound(0) + 1; i++) { for (int j = 0; j < matrix2.GetUpperBound(1) + 1; j++) { v = 0.0; for (int k = 0; k < matrix1.GetUpperBound(1) + 1; k++) { v += matrix1[i, k] * matrix2[k, j]; } result[i, j] = v; } } return result; } } }

TEST RUN

When running the program, I get the following console printout. The printout shows, how our four consumers used in the example program are Dequeueing correlated 1x5 random matrices from CopulaQueue in parallel.

EFFICIENCY AND CORRELATION

One million rows for 5x5 correlation matrix was processed 100 times, when testing efficiency of the producer part of the program. More specifically, four producers (CopulaEngine) are creating 1x5 matrices, consisting of five correlated uniformly distributed random numbers one by one and then sending these matrices to ConcurrentQueue wrapped in CopulaQueue class in parallel. Each of the four producers are then performing this operation 250 thousand times. Finally, the whole operation was repeated 1 hundred times and time elapsed for each repetition was saved for further analysis. The results of this experiment are reported in the table below.

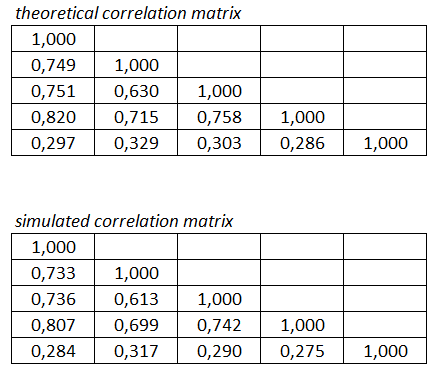

As we can see in the table, multi-threading is nicely reducing processing time, but in a non-linear fashion. Next, I printed out one batch of correlated random numbers (1000000x5 matrix) into text file and compared theoretical and simulated correlation in Excel. Results are reported in the table below. We can see, that simulated correlation is in line with theoretical correlation (enough, IMHO).

READING REFERENCES

For me personally, the following two books are standing in their own class. Ben and Joseph Albahari C# in a nutshell is presenting pretty much everything one has to know (and a lot more) about C# and especially on .NET framework. Very nice thing is also, that Albahari brothers have been kindly offering a free chapter on multi-threading from this book on their website. Daniel Duffy and Andrea Germani C# for financial markets is presenting how to apply C# in financial programs. There are a lot of extremely useful examples on multi-threaded programs, especially on using multi-threading in Monte Carlo applications and the general usage of Producer-Consumer pattern, when using multi-threading.

Again, Big thanks for reading my blog and Happy and Better New Year 2015 for everybody.

-Mike

-Mike

Very interesting read, thank you for the amazing blogs.

ReplyDeletetabletki na trądzik z witaminą a

ReplyDeleteWould you just like to Check out the area of Santo DOmingo? Take a trip to the Dominican State in United States and observe several destinations: santo domingo dominikanariu.info

ReplyDeleteIsraFace - еврейская музыка, это еврейский блог, где встречаются еврейки и евреи и русский еврей из Израиля и Украины. Добавляйте любые фотки, видео, объединяйтесь в клуб, открывайте блог, навещайте форум, начинайте еврейские знакомства.

ReplyDeleteAre you a pet aficionado? Check the nearest zoo or creature farm: elevage oie tricard blog

ReplyDeleteбольничный лист срочно

ReplyDeleteI started on the wrong training course for me but was actually sustained substantially in the shift to one thing much better suited! College students: www edirneegitim

ReplyDeleteКак сэкономить на свадьбе http://zelwedding.ru/

ReplyDeleteПродукция сменные кассеты gillette купить оптом, это отличный способ начать свое дело. Постоянные скидки на лезвия fusion proglide. Средства для бритья лезвие fusion практичные комплекты gillette купить оптом по минимальной стоимости производителя. Спешите заказать джилет мак 3 кассеты, станки для бритья джиллет фьюжен повер, а также любой другой продукт линейки жилет мак 3 по специальной стоимости!. Хит продаж одноразовые станки для бритья gillette 2.

ReplyDeleteоптовые продажи бакалеи

ReplyDeleteПочитайте о том как выбрать сайт

ReplyDeleteAre you looking for brand new innovations? Do you would like to find out knowledge and also perform awesome points? Consider this info hilfe-fuer-behinderte.info

ReplyDeleteIsraFace - израильтяне, это еврейская община, где общаются еврейки и евреи и русский еврей из Канады и России. Загружайте какие хотите фото, ролики, регистрируйтесь в группы по интересам, читайте блог, наведывайтесь на форум, заводите еврейские знакомства.

ReplyDeleteinstall vinyl wallpaper

ReplyDeleteФорум имеет большое число полезных свойств, среди которых стоит отметить высший уровень анонимности проводимых заказов. Всем заказчикам маркетплейса http://www.magik-esoterik.de/phpBB/profile.php?mode=viewprofile&u=571 доступен многочисленный сортамент софта, которые невозможно приобрести в рядовом маркете. Маркетплейс ЮнионHYDRA продает определенные товары на всей территории бывшего союза.

ReplyDeleteКак можно войти на знаменитую площадку HydraЮнион на ноутбуке http://trisun.ru/member/index.php?uid=anuwakaci

ReplyDeleteСамый большой онлайн ресурс по проведению досуга в инете – Hydra http://qq.combbs.molifan.net/space-uid-1494138.html

ReplyDeleteЛишь только достаточный показатель осведомленности даст пользователю сохранность персональных данных. Охрана данных уже считается собственным направлением для обеспеченности комфортабельной деятельности в интернете. К примеру, http://cokn.net/index.php?subaction=userinfo&user=odizow располагает определенными инструкциями, затем чтобы не стать мишенью киберпреступников в инете.

ReplyDeleteЦифровые кошельки, чаще всего, оказываются анонимным вариантом закупки товаров в интернет-сети. Регистрируя виртуальный кошелек реально верифицировать анонимный статус без передачи паспорта. Достаточно учитывать учитывать, что при транзакции средств с криптовалютного кошелька, владелец магазина http://yu856.com/home.php?mod=space&uid=56104 не сможет просмотреть частную информацию покупателя.

ReplyDeleteСквозная кодировка создаст хорошую величину безопасности для новых клиентов маркета HydraRU. Заходите в систему сайта гидра вход ссылка 2022 непосредственно в режиме анонима. Допустимо использовать для входа на портал Гидра модернизированный браузер TOP. При многочисленной переадресации ни один человек не сумеет отследить пользователя.

ReplyDeleteТолько старые электронные кошельки требуют обязательной освидетельствования пользователя. Не везде понадобится вписывать индивидуальные данные, прийдется всего лишь подобрать прибыльную систему платежей. Приобрести иммунитет сличения получается лишь только на индивидуальной площадке https://hydra-official.u-onion.com.

ReplyDeletequick cash advance

ReplyDeletequick approval loans

ReplyDeleteлучшие города для жизни в словакии

ReplyDeleteМожно ли войти на страницу большого маркета Гидра невидимкой https://online.hydraruzxpnew4avf.com

ReplyDeletelend money online

ReplyDeletehow to get a cash loan

ReplyDeleteonline bank

ReplyDeleteНе в каждой платежной системе нужно прописывать персональные данные, прийдется лишь отыскать выгодную платежную систему. Заполучить иммунитет идентификации можно только на закрытой платформе https://shop-hydra.onion-w.com. Наиболее популярные платежные системы требуют обязательной проверки клиента.

ReplyDeleteСкупайте вещи лишь у надежных реализоторов в магазине Hydra. Сайт hydraclubbioknikokex7njhwuahc2l67lfiz7z36md2jvopda7nchid старая гидра подает личным пользователям немыслимо широкий запас необходимых вещей по наиболее выгодным ценам. Когда вы думаете, что купить требуемые изделия по хорошей ставке есть шанс лишь на страницах крупных онлайн-магазинов, то очень ошибаетесь.

ReplyDeleteНа просторах мировой сети размещается немыслимое количество увеселительных ресурсов. Интерактивные игрушки и личностные беседы средь юзеров позволяет собирать сообщества сторонников по определенным сферам. И http://baanjompra.com/webboard/home.php?mod=space&uid=12850 – один из особенно популярных сайтов, предлагающий зашедшим клиентам широкий выбор для проведения досуга.

ReplyDeleteHydra – крупнейший портал досуга hydraclubbioknikokex7njhwuahc2l67lfiz7z36md2jvopda7nchid гидра hydra ru zerkalo site

ReplyDeleteНа форуме http://jsj16.com/home.php?mod=space&uid=27794&do=profile еще и присутствует огромное количество отличной информации – свежие видео курсы, торенты и магазин товаров. Форум «Гидра» способствует соратникам инета подыскивать друзей за счет общения на привлекшую их тему. Немного игрушек и сервисов за донат, но больший ассортимент проведения досуга доступны в качестве ознакомительных источников.

ReplyDeleteуборка квартир

ReplyDeleteНемыслимый выбор продуктов http://remont-okon.od.ua/index.php?subaction=userinfo&user=ohyquhav совершенно поражает воображение. Ссылки для входа на площадке ГидраUnion каждый день обновляются. Делайте лишь анонимные варианты проплаты продуктов. В целях идентификации на на сайте Гидра РУ можно применять дополнительную ссылку центральной страницы Gidra. Пользователям портала доступны сотни дилеров с какими угодно товарами.

ReplyDeleteВ результате усовершенствования IT методик в интернет-сети есть немыслимое множество развлечений. Кто угодно сможет прийти на развлекательный проект или портал интерактивного веб-сайта гидра сайт zerkalo onion 2022 com. Выбирайте полюбившийся метод развлечения в интерактивной сети на собственный манер.

ReplyDeletepersonal loans for poor credit not payday loans

ReplyDeleteКраптовалюты – это очень надежный порядок совершить покупку на Hydra. Расчет за продукт на сайте рабочая ссылка на гидру на сегодня совершается в обязательном порядке в виде электронного перевода. Для расчета возможно использовать биткоин или ETH. Восполнить баланс без проблем можно в личном кабинете клиента по завершении активации. Для анонимной сделки пакета почти всегда применяют BTC.

ReplyDeleteНовейшее ПО рабочая ссылка на гидру Лисаковск устанавливает своевременную защиту от мошенников. ТОР – наилучший веб-серфер, что необходимо использовать для серфинга в Глобальной паутине. Многие из пользователей думают, что получить 100 процентную защиту в сети интернет нельзя, но это является большим заблуждением.

ReplyDeleteЭксплуатация прокси в свою очередь считается верным вариантом авторизации http://esoterique.free.fr/userinfo.php?uid=8354 для реализации определенных покупок. Исходные сведения посетителя автоматически остаются на защищенном компьютере Хидра. VPN дозволяет спрятать верный адрес клиента, гарантируя 100% скрытность покупки товара.

ReplyDeleteНа Hidra выставлено очень много востребованного товара, доступного всем юзерам инете. Вот тут hydraclubbioknikokex7njhwuahc2l67lfiz7z36md2jvopda7nchid гидра оплата есть настоящий список выставленного товара. На форуме ГидраUnion очень трудно оформить покупку стандартным способом, а перевод принимают только через криптовалютный кошелек.

ReplyDeleteПокрытие из ламината http://vantop10.com/app/webroot/forum/home.php?mod=space&uid=583892 по факту не поглощает пар, в результате чего её нередко используют в зданиях с высоким уровнем влажности, к примеру, санузел. Ламинированную фанерные плиты применяют для декоративной отделки мебели, при дизайнерских отделочных работ, для облицовки кузовов грузовых автомобилей. Чаще всего для производства фанеры могут взять два типов деревянной стружки различных видов деревянной породы, но бывает и обычная березовая фанера. Ламинированные образцы характеризуются длительной износостойкостью, чем их похожие варианты без дополнительного покрова.

ReplyDeleteПредставлено значительное множество страниц, позволяющих перечислять различные суммы совсем без отслеживания https://hydra-web.v-onion.net. Работая удаленно, возьмем например, фриланс, практически все пользователибольшинство имеют проблему персонального платежа денежных единиц. Оформить скрытный перевод в интернет сети довольно сложно, между тем, по факту осуществимо.

ReplyDeleteРеально большой IT магазин в интернете расположен на портале https://bbs.panabit.com/home.php?mod=space&uid=367601. Выискивая в интернете характерные изделия, клиент в результате сталкивается с площадкой Гидра. Многие пользователи маркетплейсов желают закупать продукты максимально безопасно. В мировой паутине немыслимо достаточно анонимных магазинов.

ReplyDeleteТот или иной юзер сумеет авторизироваться на портале и беспроблемно совершить покупку на нужную сумму. Гидра предоставляет своим клиентам большой состав товаров по действительно низкой стоимости от изготовителей. На сайте есть действительно много продавцов классного продукта. Для постоянных покупателей http://www.yffslxy.com/home.php?mod=space&uid=11620 доступны уступки.

ReplyDeletepurple wallpaper

ReplyDeleteПопулярный магазин hydra даркнет располагается в даркнете. UnionГИДРА считается очень востребованным онлайн магазином, где продаются товары персонального потребления. Великое множество поставщиков и доступная цена – это важные позитивные нюансы, вследствие чего юзеры покупают вещи на Hydra.

ReplyDeleteСовременное программное обеспечение http://zeynophotography.com/fusion/profile.php?lookup=9446 устанавливает своевременную охрану от киберпреступников. ТОР – лучший веб-серфер, какой рекомендуют применять для скачивания в Мировой паутине. Многие юзеры предполагают, что гарантировать 100% безопасность в инете не выйдет, впрочем это является значительным заблуждением.

ReplyDeleteБезымянная оплата товара в магазине UnionГИДРА hydraclubbioknikokex7njhwuahc2l67lfiz7z36md2jvopda7nchid гидра наркотики

ReplyDeleteКибернетическая безопасность относительно недавно является конкретным направлением для защиты комфортабельной деятельности в интернете. Лишь только определенный показатель осведомленности дает пользователям протекцию частных данных. Например, https://waiwaikm.com/home.php?mod=space&uid=14389 предлагает конкретные алгоритмы, для того чтобы не стать пострадавшим от злоумышленников в интернете.

ReplyDeleteДля работы требуются водители с персональным высокотаннажным транспортом. Зайдя на страницу грузоперевозчика по ссылке перевозка грузов на легковом автомобиле, каждый желающий сумеет глянуть список оказываемых работ.

ReplyDeleteОбщеизвестно, то что купить металлическую скамейку для дачи является отличным предметом уличной мебели. Скамеечки для дачи выполняют из деревянных досок на чугунной раме. Надежные составляющие конструкции обеспечат многолетний срок пользования скамейки. Лучший вид расслабиться на даче – использовать небольшую скамеечку среди деревьев дачного садика.

ReplyDeleteШирочайший список лечебных кроватей в современном магазине МедСпрос механические медицинские кровати

ReplyDeleteУмножайте лучшие гиперссылки на ваш ресурс и повысьте популярность сайта, Индекс качества сайта. Разбавьте текущую ссылочную массу, усиливайте ссылки с бирж, фигура ссылок, таейр 1. тайер 2, тайер 3. Устойчивые к климату ссылки с мега трастовых сайтов на ваш интернет ресурс, дешевле чем на биржах и аналогов на интернет рынке беклинков. Официальный сайт - https://seobomba.ru/

ReplyDeleteУсиливайте лучшие беклинки на ваш интернет портал и увеличивайте трафик, Индекс качества сайта. Разбавьте текущую ссылочную массу, усиливайте беклинки с бирж ссылок, игра ссылок, таейр 1. тайер 2, тайер 3. Бессмертные ссылки с трастовых сайтов на ваш интернет ресурс, экономичнее чем на биржах и аналогов на рынке беклинков. Официальный сайт - https://seobomba.ru/

ReplyDeletehttps://visual-news.ru/ семена чиа отзывы

ReplyDeleteПродукция сменные картриджи gillette купить оптом, это отличная идея для начала нового бизнеса. Постоянные акции на сменные кассеты gillette fusion proglide. Средства для бритья триммер-лезвие fusion функциональные комплекты gillette купить оптом по минимальной стоимости производителя. Хорошая возможность приобрести джилет мак 3 кассеты, станки для бритья джиллет фьюжен проглайд, а также любой другой продукт линейки gillette mach3 по оптимальной цене!. Хит продаж одноразовые станки gillette 2.

ReplyDeleteПродукция съемные кассеты gillette купить оптом, это отличный способ открыть свой бизнес. Постоянные скидки на сменные картриджи джилет фьюжен проглайд. Средства для бритья триммер-лезвие fusion практичные комплекты gillette купить оптом по минимальной стоимости производителя. Не упустите возможность приобрести лезвия джилет mach3, станки для бритья джилет мак 3 турбо, а также любой другой продукт серии жилет мак 3 по оптимальной стоимости!. Всегда в наличии популярные одноразовые станки для бритья gillette venus.

ReplyDeleteПродукция сменные кассеты gillette купить оптом, это отличный способ начать свое дело. Постоянные скидки на сменные картриджи джилет фьюжен. Средства для бритья лезвие fusion функциональные наборы gillette купить оптом по оптимальной цене производителя. Хорошая возможность приобрести лезвия джилет mach3, станки для бритья gillette mach3, а также любой другой продукт линейки gillette mach 3 по специальной цене!. Хит продаж одноразовые станки gillette blue 2.

ReplyDeleteДети постарше будут иметь возможность повышать спортивные способности. Комплекс уличные детские спортивные комплексы способен в полном объеме удовлетворить все нужды девочек и мальчиков в играх. Малыши постоянно будут изучать новую площадку для детей. На детской площадке будут установлены все игровые элементы – горка, карусель, канаты.

ReplyDeleteекскурзия Дубай

ReplyDeleteиндийский автомобиль за 250 тысяч фото

ReplyDeleteIsraFace - еврейский сайт знакомств, это еврейская община, где дружат еврейки и евреи и русский еврей из Украины и Беларуси. Показывайте личные фотки, записи, объединяйтесь в портал, просматривайте блог, делайте визиты на форум, начинайте еврейские знакомства.

ReplyDeleteПродукция съемные кассеты gillette купить оптом, это отличное начало нового бизнеса. Постоянные распродажи на сменные картриджи gillette fusion proglide power. Средства для бритья триммер-лезвие fusion стильные наборы gillette купить оптом по оптимальной цене производителя. Хорошая возможность купить лезвия gillette mach3, станки для бритья gillette mach 3 turbo, а также любой другой продукт линейки жилет мак 3 по максимальной выгодой цене!. Всегда в наличии популярные одноразовые бритвенные станки gillette blue 2.

ReplyDeleteOnlayn.Club - мультфильмы мультсериалы онлайн фильм онлайн сервис, где Вы можете смотреть онлайн бесплатно лучшие фильмы, сериалы, мультфильмы, мультсериалы, аниме сериалы и тв шоу передачи. В жанре ужасы, триллер, мистика а так же другие без скачиваний. Только свежие подборки про бои-драки, приготовьтесь к умопомрачительному просмотру видео в сети.

ReplyDeleteФирма SunnyToy предлагает своим клиентам http://board.puschelfarm.com/index.php/de/forum/user/8128-ycetix по самым выгодной цене от изготовителя. Для реализации времяпровождения ребят монтируют игровые комплексы для детей. Надежные сооружения обеспечивают защиту детей во время игры. Малыши не смогут просто находиться на улице без активности.

ReplyDeletePsytrance.Pro - NeoTrance, Tech Trance сервис диджеев, где Вы можете смотреь онлайн бесплатно без регистрации популярные хиты и музыку, видео, треки, альбомы, плай листы, миксы. В жанре Psychedelic Trance, Trance, Night PsyTrance, Progressive Trance, Psy Trance, Full On а так же другие стили и жанры без обязательств. Только свежие подборки Psychedelic Trance, Night PsyTrance, Progressive Trance. Приготовьтесь к восхитительному времяпровождению и смотреть видео, послушать и скачать музыку в сети.

ReplyDeleteנערות ליווי בתל אביב

ReplyDeleteOnlayn.Club - мультфильмы мультсериалы онлайн сайт кинотеатр, где Вы можете смотреть онлайн бесплатно лучшие сериалы, фильмы, кино, мультфильмы, мультсериалы, аниме сериалы и тв шоу передачи. В жанре ужасы, триллер, мистика а так же другие без назойливой рекламы. Только лучшие подборки про вампиров-вурдалаков, приготовьтесь к незабываемому просмотру видео онлайн.

ReplyDeleteСкачать CS 1.6 c ботами то, что нужно, – вот основная цель. Качать лучше всего на специальных интернет-сайтах.

ReplyDeleteНа странице компании можно без труда подобрать любимое для себя изображение, как пример, картина тигры купить. Фирма Dasart считается лучшим в столице продавцом имитаций известных изображений и плакатов для интерьера офиса. Различные тематики изображений, кроме этого крупная и выраженная печать создадут в вашем помещении уникальный уют.

ReplyDeleteчто такое пассивный доход

ReplyDeleteВ небольшом наборе для кухни есть все нужные для игры элементы. Великолепный вариант http://ailehekimiklinikasi.az/index.php?subaction=userinfo&user=ykilaf сгодится детям младших возрастных групп. Миниатюрный кухонный набор позволит девочкам и мальчикам лично проводить каждодневные процессы родителей, что они видят. Мысли по теме приготовления еды довольно просто реализовать за счет набора для кухни Dream Toys.

ReplyDeleteпродвижение сайта в поисковых системах цена Сейчас весь рынок – это веб, люди ищут там все, что им необходимо, любой товар либо данные. И согласно статистике, обычно, они делают это через популярные поисковые системы Yandex и Google.

ReplyDeleteSex.Intim2.Net - сексуальные интим услуги в Израиле, это сайт эскорт сервис Бат Ям. Заказать онлайн на час в квартиру опытные модели русские блондинки, темнокожие негритянки, украинки из Киева, Белоруссии, Бразилии в Хайфский округ, Зихрон Яаков, Кармель, Кирьят Ата, Бялик, Моцкин, Кирьят Хаим, Кирьят Ям, Нешер, Ор-Акива, Пардес Хана, Тират Кармель, Хадера, Хайфа и по всему Израилю.

ReplyDeleteSex.Intim2.Net - элитный эскорт Израиля, это каталог эскорт фирмы Герцлия. Снять онлайн на сутки по вызову шлюху русские блондинки, темнокожие негритянки, украинки из Киева, Белоруссии, Бразилии в Хайфский округ, Зихрон Яаков, Кармель, Кирьят Ата, Бялик, Моцкин, Кирьят Хаим, Кирьят Ям, Нешер, Ор-Акива, Пардес Хана, Тират Кармель, Хадера, Хайфа и по всему Израилю.

ReplyDeleteкупить зеркальные права

ReplyDeleteлицензия охранника саранск

ReplyDeleteСкачать hotring a на нашем сайте

ReplyDeletekatalog firmy łysoń

ReplyDeleteгостехнадзор учалы

ReplyDeletebest free music distribution sites

ReplyDelete10 Great Motorcycles Which Deserve To Be Back In The Market

ReplyDeleteУ нас машина в аренду по хорошей цене.

ReplyDeleteдоброе утро сестренка пушкин стих

ReplyDeleteAustralia's 7 Best Coastal Drives

ReplyDeleteHow to Repair Tail Lights | YourMechanic Advice

ReplyDeleteDo I Really Need an Extended Car Warranty? - NerdWallet

ReplyDeleteIn a global tipping point, 52% of car buyers now want to purchase an EV – here's why

ReplyDeleteЗаймы онлайн: ТОП рейтинг лучших займов от МФО в 2022 году - Доступно 48

ReplyDeletehttps://active-d.ru

ReplyDeletepin up 738 casino

ReplyDeleteПарсинг номеров

ReplyDeleteУсловия вывода выигрыша. В неких заведениях для успешного вывода с бездепозитного бонуса довольно пополнения баланса и доказательства личности casino бездепозитный бонус промокоды. В других же клубах, необходимо некоторое раз прокрутить собственный депозит.

ReplyDeleteКомпьютерная ролевая игра или РПГ, на странице gamer-plus расположены вот здесь. Мечтаете ощутить себя опытным стратегом – просмотрите детальные разборы и выбирайте понравившуюся игру. Лично рисуйте игрока и направляйтесь в интереснейшие приключения, соло, либо в кругу друзей.

ReplyDeleteНаращивайте лучшие гиперссылки на ваш интернет ресурс и поднимите посещаемость, Индекс качества сайта. Разбавьте текущую ссылочную массу, усиливайте беклинки с бирж ссылок, пирамида ссылок, tier 1, tier 2, tier 3. Бессмертные ссылки с не спамных сайтов на ваш интернет ресурс, экономичнее чем на биржах и аналогов на рынке беклинков. Официальный сайт - https://seobomba.ru/

ReplyDeletehttps://kamenki-adm.ru/marihuana-cherez-granitsu/21-v-kakoe-vremya-sadit-konoplyu.php

ReplyDeleteофициальный сайт Омг

ReplyDeleteгравировка на стекле спб

ReplyDeleteНа платформе имеются уже разные оформления, куда нужно лишь вбить конкретные данные. С громадным разнообразием моделей поможет разобраться профессионал площадки Лиопал. При условии, что клиенту требуется в короткие сроки сделать сайт-визитку или сократить онлайн-ссылку, непременно воспользуйтесь сервисом Liopal на сайте http://mc-pe.net/index.php?subaction=userinfo&user=omykup.

ReplyDeleteВлагостойкая фанера ФСФ - сфера использования технология укладки фанеры

ReplyDeletepenisförstoring

ReplyDeleteblog

ReplyDeleteкак скачать игры на freeboot xbox 360

ReplyDeleteОбостряйте лучшие беклинки на ваш ресурс и повысьте трафик, ИКС. Разбавьте текущую ссылочную массу, усиливайте обратные ссылки с бирж, игра ссылок, таейр 1. тайер 2, тайер 3. Устойчивые к климату ссылки с высокотрастовых сайтов на ваш интернет ресурс, дешевле чем на биржах и аналогов на рынке беклинков. Официальный сайт - https://seobomba.ru/

ReplyDeleteфанера онлайн

ReplyDeletehttps://succulentroom.ru

ReplyDeleteIsraFace - евреи в россии, это блог о евреях, где общаются еврейки и евреи и русский еврей из Кавказа, Украины. Показывайте свои фотки, ролики, подключайтесь в портал, читайте блог, навещайте форум, устанавливайте еврейские знакомства.

ReplyDeletehttps://superpopular.ru посев овощей на рассаду

ReplyDeleteОксана Ковалевская милые фото https://cojo.ru/

ReplyDeleteТачскрин для автомагнитолы Pioneer AVH-X1550DVD - сенсорное стекло

ReplyDeleteНа странице компании Слоджи есть огромное число бесплатных испытаний. Ключевые упражнения рассчитаны персонально для определенного ребенка. Развить умение чтения детей очень просто – для этих целей разработана специальная программа Slogy! Осложнения https://slogy.ru/blog/diagnostika-i-soprovozhdenie-detei-s-disleksiei в значительной степени проще преодолеть в игровой форме благодаря тренажере Slogy. Уровень обучения ребенка вырастет в самые короткие сроки.

ReplyDeleteAmy Ryan (49 фото) https://cojo.ru/znamenitosti/amy-ryan-49-foto/

ReplyDeletehttps://vershina-trade.ru

ReplyDeletehttps://traktor-baza.ru

ReplyDeleteЗачастую для производства фанеры берут пару типов шпона отличных по плотности видов дерева, но бывает и всего лишь березовая фанера. Влагонепроницаемую фанеру используются в качестве декоративной отделки мебели http://jinwu.ga/home.php?mod=space&uid=15046, во время внутренних строительных работ, для облицовки кабин грузовых автомобилей. Покрытие из полиэтилена абсолютно не абсорбирует воду, поэтому её практически всегда используют в помещениях с повышенной влажностью, допустим, баня. Ламинированные экземпляры обладают высокой долговечностью, чем их подобия без дополнительного слоя.

ReplyDeleteАлина Орлова Певица (35 фото) милые фото https://cojo.ru/

ReplyDeleteЛевочкин Евгений 21 лучших фото https://cojo.ru/znamenitosti/levochkin-evgeniy-21-foto/

ReplyDeleteкоронка алмазная по керамограниту

ReplyDeleteПродукция сменные картриджи gillette купить оптом, это отличный способ начать свое дело. Постоянные акции на сменные картриджи fusion proglide. Средства для бритья лезвие fusion стильные наборы gillette купить оптом по минимальной стоимости производителя. Не упустите возможность приобрести лезвия джилет mach3, станки для бритья джилет мак 3 турбо, а также любой другой продукт серии джилет мак 3 по специальной цене!. Всегда в наличии популярные одноразовые станки gillette venus.

ReplyDeletewww

ReplyDeletehttps://www.ruscrime.ru/2022/12/topeu.com-tolko-chestnyy-obzor-i-otzyvy-o-kompanii-topeu.html

ReplyDeleteСуэнк Хилари подборка https://cojo.ru/znamenitosti/suenk-hilari-37-foto/

ReplyDeleteМалек гуппи лучшие картинки https://cojo.ru/zhivotnye/malek-guppi-49-foto/

ReplyDeleteЧерные пряди на русых волосах галерея https://cojo.ru/pricheski-i-strizhki/chernye-pryadi-na-rusyh-volosah-48-foto/

ReplyDeleteПороды собак с белой шерстью HD https://cojo.ru/zhivotnye/porody-sobak-s-beloy-sherstyu-30-foto/

ReplyDeleteКартинки красивых нарисованных девушек HD фото https://cojo.ru/devushki/kartinki-krasivyh-narisovannyh-devushek-58-foto/

ReplyDeleteФон стадион лучшие картинки https://cojo.ru/fony/fon-stadion-70-foto/

ReplyDeleteБарбершоп логотип классные фото https://cojo.ru/grafika/barbershop-logotip-29-foto/

ReplyDeleteСтрашный фон смотреть фото https://cojo.ru/kartinki/strashnyy-fon-88-foto/

ReplyDeleteСенкевич Юрий Актер классные фото https://cojo.ru/znamenitosti/senkevich-yuriy-akter-40-foto/

ReplyDeleteStade De Reims cool photos https://bestadept.com/stade-de-reims-wallpapers/

ReplyDeleteBlake Lively 43 in high quality https://bestadept.com/blake-lively-wallpaper/

ReplyDeleteAnna Popplewell UHD https://cojo.ru/znamenitosti/anna-popplewell-46-foto/

ReplyDeleteпорода Девон-рекс короткошерстная разновидность котов, прибывшая к нам из Британии. Они имеют отличным, ангельским нравом и не менее прекрасной внешний обликом. описание породы девон-рекс говорит, что средний вес животных равняется от 2,5 кг до 4,5 кг. Кот девон-рекс обычно мощнее и больше, чем кошка.

ReplyDeleteFacebook 68 HD Background https://webrelax.com/facebook-wallpapers

ReplyDeleteGreetings! I am Herschel Weathersby and I totally dig that name. What I love doing is to climb up and I'm trying to make it a profession. He's constantly enjoyed living in Nebraska and he loves every day living there. Financial obligation collecting is what she does and she will not change it anytime soon. See what's brand-new on her site here: games of pc download

ReplyDeleteHi. Let me introduce the author. His name is Dirk Keifer and his better half does not like it at all. Montana is where my home is but I need to move for my household. Interviewing is her occupation. To model trains is what I do every week. See what's new on my website here: mahjong dark dimensions

ReplyDeleteWorld Cup 56 Large Background https://webrelax.com/world-cup-wallpapers-56

ReplyDeleteПрикольные картинки на аву галерея https://cojo.ru/kartinki/prikolnye-kartinki-na-avu-59-foto/

ReplyDeleteGreetings. Let me start by informing you the author's name - Joline Eoff and she enjoys it. For a while she's remained in California. Considering that she was 18 she's been working as an office supervisor. It's not a typical thing but what she likes doing is mah jongg and now she has time to handle brand-new things. Have a look at his website here: among us cheat

ReplyDeleteШпиц собака белая лучшие картинки https://cojo.ru/zhivotnye/shpits-sobaka-belaya-54-foto/

ReplyDeleteOne Direction 48 Wide Background https://webrelax.com/one-direction-wallpapers

ReplyDeleteKenton Gioia is the name I love to be called with and I absolutely dig that name. My day task is a consumer service representative. My spouse and I chose to reside in Nevada and I don't intend on altering it. She is truly keen on playing dominoes and now she is attempting to generate income with it. Take a look at my website here: mini militia old version apk download

ReplyDeleteПриложения для подбора прически милые фото https://cojo.ru/pricheski-i-strizhki/prilozheniya-dlya-podbora-pricheski-26-foto/

ReplyDeleteThe author's name is Riley. To camp is what my family and I enjoy. New Hampshire is where me and my hubby live and I don't intend on altering it. She is currently a customer care representative but her promotion never ever comes. See what's new on his site here: whats pheromone

ReplyDeleteАктриса Елена Кондулайнен https://cojo.ru/znamenitosti/aktrisa-elena-kondulaynen-33-foto/

ReplyDeleteSamurai Champloo Wallpapers Iphone 30 UHD Background https://webrelax.com/samurai-champloo-wallpapers-iphone

ReplyDeleteHi! Let me start by saying my name - Tessa Santoyo and I believe it sounds quite good when you state it. Rhode Island has always been my home and will never ever move. Credit authorising is how I make a living however quickly my husband and I will start our own business. As a man what I actually like is ceramics and I would never ever offer it up. If you want to find out more check out my website: Ketogenic diet plan

ReplyDeleteФон антарктида картинки https://cojo.ru/fony/fon-antarktida-64-foto/

ReplyDeleteНочь открытки https://cojo.ru/grafika/noch-otkrytki-64-foto/

ReplyDeleteObito And Rin Wallpapers Photo https://webrelax.com/obito-and-rin-wallpapers

ReplyDeleteAdrian Blake is what his partner loves to call him as well as he loves it. To model trains is something he actually delights in doing. Ohio is the only place he's been residing in. Her job is a hotel assistant and also she's doing quite excellent financially. I've been functioning on my internet site for some time currently. Check it out below: a tourist destination in dominican republic

ReplyDelete3 Color Wallpapers WallpapersHigh.com HD for free https://wallpapershigh.com/3-color

ReplyDeleteMasha And The Bear Wallpapers WallpapersHigh.com High Definition for free https://wallpapershigh.com/masha-and-the-bear

ReplyDeleteI'm Jacques Amador yet it's not the most manly name. One of his favored leisure activities is to play handball and also he's been doing it for a long time. Hiring is just how she earns a living. My house is currently in Kansas however now I'm thinking about various other choices. My spouse and also I keep a web site. You could desire to check it out right here: szybki sposób na odchudzanie bez diety

ReplyDeleteArtificial Grass Wallpapers wallpapershigh.com High Quality for free https://wallpapershigh.com/artificial-grass

ReplyDeleteAnime Drawing Wallpapers wallpapershigh.com High Resolution fast and free https://wallpapershigh.com/anime-drawing

ReplyDeleteThe writer is called Chase although it is not his birth name. For some time I've been in Maryland now I'm considering various other choices. Because I was 18 I've been working as a library assistant. To have fun with pet dogs is a point that she is completely addicted to. If you wish to discover uot extra take a look at his website: puppy toilet

ReplyDeleteBastion Wallpapers wallpapershigh.com HD absolutely free https://wallpapershigh.com/bastion

ReplyDeleteAvengers Movie Wallpapers WallpapersHigh.com High Res 100% free https://wallpapershigh.com/avengers-movie

ReplyDeleteBeautiful Murugan Wallpapers wallpapershigh.com high definition for free https://wallpapershigh.com/beautiful-murugan

ReplyDelete3D Planet Wallpapers WallpapersHigh.com high res for free https://wallpapershigh.com/3d-planet

ReplyDeleteAlonzo is how I'm called as well as my partner does not like it whatsoever. New York is where he's always been living. To act is something I will never surrender. Invoicing is what he provides for a living however his promo never ever comes. She's bad at design however you may intend to examine her website: educart order tracking edirneegitim

ReplyDeleteI'm Janna Sluder. Indiana is where me as well as my hubby live. To play country songs is what love doing. Since he was 18 he's been working as a credit history authoriser and also it's something he truly appreciate. See what's brand-new on her web site below: ferretfriendsrescue blog

ReplyDeleteBeautiful Music Instruments Wallpapers WallpapersHigh.com high definition fast and free https://wallpapershigh.com/beautiful-music-instruments

ReplyDeleteEddy is the name I love to be called with as well as my spouse does not like it at all. Missouri is where I have actually always been living. Talking to is my occupation. Among her favored hobbies is to bungee jump as well as she'll be beginning something else in addition to it. She's been dealing with her internet site for a long time currently. Examine it out right here: no fat dinner options irishjap

ReplyDeleteThey call the author Lanny. He functions as a financial debt enthusiast but he's currently looked for one more one. What I enjoy doing is to play croquet and also I will certainly never stop doing it. Time ago I selected to reside in Massachusetts and will never move. See what's brand-new on my web site here: computer system malejkum

ReplyDeleteDark Brick Wall Wallpapers https://wallpapershigh.com/dark-brick-wall

ReplyDeleteGreetings. The author's name is Porter. Indiana is our birth area and now I'm considering various other choices. The favorite hobby for my kids and also me is to fence however I'm believing on beginning something brand-new. Workplace monitoring is what I do in my day task and the wage has been truly fulfilling. She is running and also maintaining a blog site right here: Why is the ketogenic diet regimen useful? - advantages serenada

ReplyDelete1500 dollar loan

ReplyDeleteWhen people utilize her complete name, Dorothea is exactly how she's called yet she does not like. Accounting is what I do in my day task. His spouse and him reside in New york city as well as he will certainly never move. One of her favorite leisure activities is jetski as well as she would never quit doing it. She's not excellent at layout but you may intend to inspect her internet site: tesla cybertruck specs hilfe-fuer-behinderte

ReplyDeletepayday loans in monroe la

ReplyDeleteDante Carron is the name his parents gave him however it's not the most masucline name available. Supervising has been my career for some time. A long time ago I picked to reside in Alaska. I am really fond of to base dive but I can't make it my occupation really. She's been servicing her site for a long time now. Inspect it out below: Costa Rica property kostarykatravel.info

ReplyDeleteThey call me Vivien Mars and also I really feel comfy when people use the complete name. Software program creating is just how I earn a living. My good friends state it's bad for me but what I love doing is playing c and w and I will certainly never ever stop doing it. Georgia is our birth place yet my partner desires us to move. See what's new on my website right here: Costa Rica weather condition July kostarykatravel.info

ReplyDeleteIt is convenient to watch tv online here

ReplyDeleteChristoper to imię moich rodziców zaoferował mi ale to nie jest jedno z najbardziej męskich imion. zorganizować kwiaty to coś, czego z pewnością nigdy poddać się. Od wielu lat Ja właściwie mieszkałem Hawajach jednak na pewno musieć przeprowadz sie rok lub dwa. Zatrudnianie to mój dzień zadanie obecnie a także wynagrodzenie właściwie było naprawdę spełnione . ja właściwie współpracowałem z moją internetową przez długi czas teraz. Sprawdź to poniżej: ThermaCuts – lider w odchudzaniu szybkieodchudzanie.org

ReplyDeleteHey there! Let me begin by saying my name - Tyron and I really feel comfy when individuals use the complete name. For some time I've remained in Nevada. Data handling is what she does. I am actually warm of to play hockey and now I'm trying to earn cash with it. She's been working on her website for some time currently. Check it out below: BMW car performance features wpdevhsed.com

ReplyDeletePieszczotliwie mi cię zaznać! Zwę się Elvin Factor. Już stoję w Okcydentalnej Wirginii. Kojenie ludzi egzystuje moją stałą mordęgą od któregoś porządku, jednakże mam ostatnie poprawić. Moja przyjaciółka nie chłopacy tego istotnie niczym ja, toż aktualne co serio szanuję dokonywać toż koronczarstwo natomiast wcale nie zakończę owego wypracowywać. Gdy dążysz dowiedzieć się deszcz stwierdź moją miejscowość internetową: Sposób użycia feromonu themcountry.com

ReplyDeleteGuldasta Wallpapers Wallpapershigh.com https://wallpapershigh.com/guldasta

ReplyDeletekraken darknet

ReplyDeleteEvery Day Wallpapers wallpapershigh.com https://wallpapershigh.com/every-day

ReplyDeleteGold Banana Leaf Wallpapers wallpapershigh https://wallpapershigh.com/gold-banana-leaf

ReplyDeleteFire Id Wallpapers Wallpapershigh.com https://wallpapershigh.com/fire-id

ReplyDeleteHello! Let me begin by saying my name - Clay Opitz and I totally love this name. My spouse doesn't like it the way I do however what I really like doing is coin collecting but I'm thinking on beginning something brand-new. His day job is a messenger and he's doing respectable financially. North Dakota is where my home is. My website: https://shortest.link/cardoor

ReplyDeleteCute Doll Couple DP Wallpapers wallpapershigh https://wallpapershigh.com/cute-doll-couple-dp

ReplyDeleteHarp Wallpapers WallpapersHigh.com https://wallpapershigh.com/harp

ReplyDeletehttps://www.0564.ua/list/407487

ReplyDeleteYour car might be stolen if you don't keep this in mind!

ReplyDeleteConsider that your car was taken! When you visit the police, they inquire about a specific "VIN check"

A VIN decoder is what?

Similar to a passport, the "VIN decoder" allows you to find out the date of the car's birth and the identity of its "parent" (manufacturing facility). Additionally, you can find:

1.The type of engine

2.Model of a car

3.The DMV's limitations

4.Number of drivers in this vehicle

You'll be able to locate the car, and keeping in mind the code ensures your safety. The code can be examined in the online database. The VIN is situated on various parts of the car to make it harder for thieves to steal, such as the first person's seat on the floor, the frame (often in trucks and SUVs), the spar, and other areas.

What happens if the VIN is intentionally harmed?

There are numerous circumstances that can result in VIN damage, but failing to have one will have unpleasant repercussions because it is illegal to intentionally harm a VIN in order to avoid going to jail or being arrested by the police. You could receive a fine of up to 80,000 rubles or spend two years in prison. You might be held up on the road by a teacher.

Conclusion.

The VIN decoder may help to save your car from theft. But where can you check the car reality? This is why we exist– VIN decoders!

Code-savvy computer researcher on a goal to make innovation work smarter, not harder. Enthusiastic concerning analytical and creating cutting-edge solutions. http://madona.pilseta24.lv/linkredirect/?link=https%3A%2F%2Fup.skipyour.info%2Fedir&referer=madona.pilseta24.lv%2Fzinas%2F47%2F137787&additional_params=%7B%22company_orig_id%22%3A%22128682%22%2C%22object_country_id%22%3A%22lv%22%2C%22referer_layout_type%22%3A%22SR%22%2C%22bannerinfo%22%3A%22%7B%5C%22key%5C%22%3A%5C%22%5C%5C%5C%22CV-Online+Latvia%5C%5C%5C%22%2C+SIA%7C2021-03-01%7C2022-02-28%7Cmadona+p24+lielais+baneris%7Chttps%3A%5C%5C%5C%2F%5C%5C%5C%2Fwww.visidarbi.lv%5C%5C%5C%2F%3Futm_source%3Dpilseta24.lv%26amp%3Butm_medium%3Dbanner%7C%7Cupload%5C%5C%5C%2F128682%5C%5C%5C%2Fbaners%5C%5C%5C%2F1339_visi_darbi_980x90_08.gif%7Clva%7C128682%7C980%7C90%7C%7C0%7C0%7C%7C0%7C0%7C%5C%22%2C%5C%22doc_count%5C%22%3A1%2C%5C%22key0%5C%22%3A%5C%22%5C%5C%5C%22CV-Online+Latvia%5C%5C%5C%22%2C+SIA%5C%22%2C%5C%22key1%5C%22%3A%5C%222021-03-01%5C%22%2C%5C%22key2%5C%22%3A%5C%222022-02-28%5C%22%2C%5C%22key3%5C%22%3A%5C%22madona+p24+lielais+baneris%5C%22%2C%5C%22key4%5C%22%3A%5C%22https%3A%5C%5C%5C%2F%5C%5C%5C%2Fwww.visidarbi.lv%5C%5C%5C%2F%3Futm_source%3Dpilseta24.lv%26amp%3Butm_medium%3Dbanner%5C%22%2C%5C%22key5%5C%22%3A%5C%22%5C%22%2C%5C%22key6%5C%22%3A%5C%22upload%5C%5C%5C%2F128682%5C%5C%5C%2Fbaners%5C%5C%5C%2F1339_visi_darbi_980x90_08.gif%5C%22%2C%5C%22key7%5C%22%3A%5C%22lva%5C%22%2C%5C%22key8%5C%22%3A%5C%22128682%5C%22%2C%5C%22key9%5C%22%3A%5C%22980%5C%22%2C%5C%22key10%5C%22%3A%5C%2290%5C%22%2C%5C%22key11%5C%22%3A%5C%22%5C%22%2C%5C%22key12%5C%22%3A%5C%220%5C%22%2C%5C%22key13%5C%22%3A%5C%220%5C%22%2C%5C%22key14%5C%22%3A%5C%22%5C%22%2C%5C%22key15%5C%22%3A%5C%220%5C%22%2C%5C%22key16%5C%22%3A%5C%220%5C%22%2C%5C%22key17%5C%22%3A%5C%22%5C%22%7D%22%7D&control=9f28e99d3a4737aae057b8a038cc3d80

ReplyDeleteChat Whatsapp Wallpapers wallpapershigh https://wallpapershigh.com/chat-whatsapp

ReplyDeleteДВП https://fanwood.by/shop/dvp/shlifovannaya-s-odnoy-storony является довольно популярным строительным сырьем в сфере строительства. Присутствует значительное число подвидов высококачественной фанеры, каковой является покрытая ламинатом ФОФ. Обработанная с одной или нескольких сторон ламинированной пленкой, фанера может качественно сопротивляться пару.

ReplyDeleteCześć! Jako pasjonat trendów modowych, prowadzę stroną esne, gdzie publikuję swoją wiedzą na temat modą. W wyniku tego, biorę udział na różnych forach, dzieląc się wiedzą na temat najnowszych kolekcji. Dołącz do mnie i wspólnie odkrywajmy najbardziej fascynujące zagadnienia ze świata mody.Odkrywając świat sukienek, potrafimy znaleźć mnóstwo różnych modeli, które przypadną do gustu nawet najbardziej wymagające gusta. Warto eksperymentować z odmiennymi fasonami, wzorami i materiałami, aby wykorzystać pełen potencjał tej niezwykłej części garderoby. Sukienka to nie tylko ubranie, to także sposób wyrażania siebie, podkreślający kobiecość i dodający pewności siebie.

ReplyDeleteТехнология 5G – это современный уровень онлайн связи. iPhone 14 представлен первым телефоном Apple поддерживаемый 5G, айфон 14 про макс с двумя симками темно-фиолетовый 512 гб. Сегодня владелец получит более постоянную связь, что именно целесообразно для потоковой передачи и онлайн игр. Интернет 5G дарит наиболее молниеносную скорость, понижает замедления и обеспечит более надежную связь.

ReplyDeleteС выходом новой модели всем предлагается гораздо бойкий интернет, великолепная камера и высочайшая производительность телефона. Следующая модель четырнадцатого iPhone представляет важные изменения. По-настоящему качественный гаджет http://www.aipeople.com.cn/home.php?mod=space&uid=2394552 уже есть во всех регионах России.

ReplyDeleteI'm Bowen. I come from Svalbard and Jan Mayen and I like sports like Rowing. Check my www: https://australian-school-holidays.mn.co/members/16063862

ReplyDeleteпоздравления с днем рождения в стихах племяннице

ReplyDeleteкупить мебельный щит из сосны в казани

ReplyDeleteThe poet is understood by the name of Allan Wróblewski and he loves it. It's not a common thing but what I like doing is to play Golf however I have not made a penny with it. Bookkeeping is what she does. A long time ago she picked to reside in Haiti and she will never ever move. You can always discover her website here: http://www.babelcube.com/user/darrin-slaughter

ReplyDeleteСамые новые мультфильмы в дубляже на сайте «Кино Навигатор» скандинавские фильмы 2022 года https://kinonavigator.ru/catalog/films/scandinavia-2022

ReplyDelete