A few words about this implementation. AlgLibLMASolver class uses AlgLib library functions (functions from 21 different modules) for processing (creating optimization model, setting conditions, processing iterations). One data member within this class is having a type of IModel. This data member is actually a reference to an interface, which provides a set of functions for all required calculations (objective function value, values for function terms, partial derivative values for function terms). Since all possible implementations for any interface method must honor signatures exactly, there is a problem with VBA since it does not have a real constructor mechanism. I have chewed this issue in here. It might help to explain the reason, why I have been distributing input parameters for interface implementation by using Dictionary object. Finally, HoLeeZeroCouponCalibration class is implementing IModel interface (a set of functions for all required calculations). In essence, algorithms (AlgLib-related processing) and data (values calculated specifically by using Ho-Lee model) have been completely separated. Needless to say, this type of scheme is flexible for new implementations.

Create a new VBA project and copy-paste the following classes and modules into this project. Also, import all required 21 AlgLib BAS files into this project.

' CLASS : AlgLibLMASolver Option Explicit ' ' The following 21 AlgLib modules are required for succesfull compilation of this project : ' ablas, ablasf, ap, bdsvd, blas, creflections, densesolver, hblas, linmin, matinv, ' minlbfgs, minlm, ortfac, rcond, reflections, rotations, safesolve, sblas, svd, trfac, xblas ' Private state As MinLMState Private report As MinLMReport Private n As Long Private m As Long Private x() As Double Private model As IModel Private epsF As Double Private epsG As Double Private epsX As Double Private iterations As Long ' Public Function initialize( _ ByVal numberOfVariables As Long, _ ByVal numberOfEquations As Long, _ ByRef changingVariables() As Double, _ ByRef callbackModel As IModel, _ ByVal epsilonF As Double, _ ByVal epsilonG As Double, _ ByVal epsilonX As Double, _ ByVal maximumIterations As Long) ' n = numberOfVariables m = numberOfEquations x = changingVariables Set model = callbackModel epsF = epsilonF epsG = epsilonG epsX = epsilonX iterations = maximumIterations End Function ' Public Sub Solve() ' ' create solver scheme using functions and analytical partial derivatives Call MinLMCreateFJ(n, m, x, state) ' set stopping conditions Call MinLMSetCond(state, epsG, epsF, epsX, iterations) ' ' process iterations Do While MinLMIteration(state) ' ' calculate value for objective function If (state.NeedF) Then ' model.callBackObjectiveFunction state End If ' ' calculate values for functions and partial derivatives If (state.NeedFiJ) Then ' model.callBackFunction state model.callBackJacobian state End If Loop ' ' process results Call MinLMResults(state, x, report) End Sub ' ' public accessor to (MinLMState) state Public Property Get GetState() As MinLMState GetState = state End Property ' ' public accessor to (MinLMReport) report Public Property Get GetReport() As MinLMReport GetReport = report End Property ' ' public accessor to hard-coded report Public Property Get GetPrettyPrintReport() As String ' Dim message As String message = "*** AlgLibLMASolver execution report " + VBA.CStr(VBA.Now) + " ***" + VBA.vbNewLine message = message + "TerminationType : " + VBA.CStr(report.TerminationType) + VBA.vbNewLine message = message + "Iterations : " + VBA.CStr(report.IterationsCount) + VBA.vbNewLine message = message + "Objective function : " + VBA.CStr(state.f) + VBA.vbNewLine message = message + VBA.vbNewLine ' Dim i As Integer For i = 0 To (state.n - 1) message = message + "x(" + VBA.CStr(i) + ") = " + VBA.CStr(state.x(i)) + VBA.vbNewLine Next i ' GetPrettyPrintReport = message End Property ' ' ' ' ' ' CLASS : IModel Option Explicit ' set of functions for IModel interface Public Function initialize(ByRef parameters As Scripting.Dictionary) ' assign required member data wrapped into dictionary End Function ' Public Function callBackObjectiveFunction(ByRef state As MinLMState) ' calculate objective function value End Function ' Public Function callBackFunction(ByRef state As MinLMState) ' calculate values for (non-squared) function terms End Function ' Public Function callBackJacobian(ByRef state As MinLMState) ' calculate partial derivative values for (non-squared) function terms End Function ' ' ' ' ' ' CLASS : HoLeeZeroCouponCalibration Option Explicit ' Implements IModel ' Private s As Double Private r As Double Private t() As Double Private z() As Double ' Private Function IModel_initialize(ByRef parameters As Scripting.IDictionary) ' s = parameters(HOLEE_PARAMETERS.sigma) r = parameters(HOLEE_PARAMETERS.shortRate) t = parameters(HOLEE_PARAMETERS.maturity) z = parameters(HOLEE_PARAMETERS.zeroCouponBond) End Function ' Private Function IModel_callBackObjectiveFunction(ByRef state As MinLMState) ' ' calculate value for aggregate objective function Dim i As Integer Dim hoLeeZero As Double Dim f As Double: f = 0 ' ' loop through number of equations For i = 0 To (state.m - 1) ' hoLeeZero = VBA.Exp(-(1 / 2) * state.x(i) * (t(i) ^ 2) + (1 / 6) * (s ^ 2) * (t(i) ^ 3) - r * t(i)) f = f + (z(i) - hoLeeZero) ^ 2 Next i state.f = f End Function ' Private Function IModel_callBackFunction(ByRef state As MinLMState) ' ' calculate values for (non-squared) function terms Dim i As Integer Dim hoLeeZero As Double ' ' loop through number of equations For i = 0 To (state.m - 1) ' hoLeeZero = VBA.Exp(-(1 / 2) * state.x(i) * (t(i) ^ 2) + (1 / 6) * (s ^ 2) * (t(i) ^ 3) - r * t(i)) state.FI(i) = (z(i) - hoLeeZero) Next i End Function ' Private Function IModel_callBackJacobian(ByRef state As MinLMState) ' ' calculate partial derivative values for (non-squared) function terms Dim i As Integer, J As Integer Dim hoLeeZero As Double ' ' 1. individual (non-squared) function terms ' loop through number of equations For i = 0 To (state.m - 1) ' hoLeeZero = VBA.Exp(-(1 / 2) * state.x(i) * (t(i) ^ 2) + (1 / 6) * (s ^ 2) * (t(i) ^ 3) - r * t(i)) state.FI(i) = (z(i) - hoLeeZero) Next i ' ' 2. partial derivatives for all (non-squared) function terms ' loop through number of equations For i = 0 To (state.m - 1) ' ' loop through number of variables For J = 0 To (state.n - 1) ' Dim derivative As Double: derivative = 0 ' partial derivative is non-zero only for diagonal cases If (i = J) Then derivative = (1 / 2) * VBA.Exp(1) * t(J) ^ 2 state.J(i, J) = derivative End If Next J Next i End Function ' ' ' ' ' ' MODULE : DataStructures Option Explicit ' Public Enum HOLEE_PARAMETERS sigma = 1 shortRate = 2 maturity = 3 zeroCouponBond = 4 End Enum ' ' ' ' ' ' TESTER MODULE Option Explicit ' ' Ho-Lee model calibration example Public Sub AlglibTester() ' ' MODEL part ' construct all required inputs and model to be calibrated Dim sigma As Double: sigma = 0.00039 Dim shortRate As Double: shortRate = 0.00154 ' Dim maturity(0 To 9) As Double maturity(0) = 1: maturity(1) = 2: maturity(2) = 3: maturity(3) = 4: maturity(4) = 5: maturity(5) = 6: maturity(6) = 7: maturity(7) = 8: maturity(8) = 9: maturity(9) = 10 ' Dim zero(0 To 9) As Double zero(0) = 0.9964: zero(1) = 0.9838: zero(2) = 0.9611: zero(3) = 0.9344: zero(4) = 0.9059: zero(5) = 0.8769: zero(6) = 0.8478: zero(7) = 0.8189: zero(8) = 0.7905: zero(9) = 0.7626 ' ' assign parameters into dictionary wrapper Dim parameters As New Scripting.Dictionary parameters.Add HOLEE_PARAMETERS.sigma, sigma parameters.Add HOLEE_PARAMETERS.shortRate, shortRate parameters.Add HOLEE_PARAMETERS.maturity, maturity parameters.Add HOLEE_PARAMETERS.zeroCouponBond, zero ' ' create and initialize calibration model Dim model As IModel: Set model = New HoLeeZeroCouponCalibration model.initialize parameters ' ' SOLVER part Dim Theta(0 To 9) As Double ' assign initial guesses Theta(0) = 0.001: Theta(1) = 0.001: Theta(2) = 0.001: Theta(3) = 0.001: Theta(4) = 0.001: Theta(5) = 0.001: Theta(6) = 0.001: Theta(7) = 0.001: Theta(8) = 0.001: Theta(9) = 0.001 ' Dim numberOfVariables As Long: numberOfVariables = 10 Dim numberOfEquations As Long: numberOfEquations = 10 Dim epsilonF As Double: epsilonF = 0.000000000001 Dim epsilonG As Double: epsilonG = 0.000000000001 Dim epsilonX As Double: epsilonX = 0.000000000001 Dim maximumIterations As Long: maximumIterations = 25000 ' ' create and initialize solver model Dim solver As New AlgLibLMASolver solver.initialize _ numberOfVariables, _ numberOfEquations, _ Theta, _ model, _ epsilonF, _ epsilonG, _ epsilonX, _ maximumIterations ' ' solve calibration model solver.Solve ' ' print hard-coded report containing values for ' objective function, variables and other information Debug.Print solver.GetPrettyPrintReport End Sub '

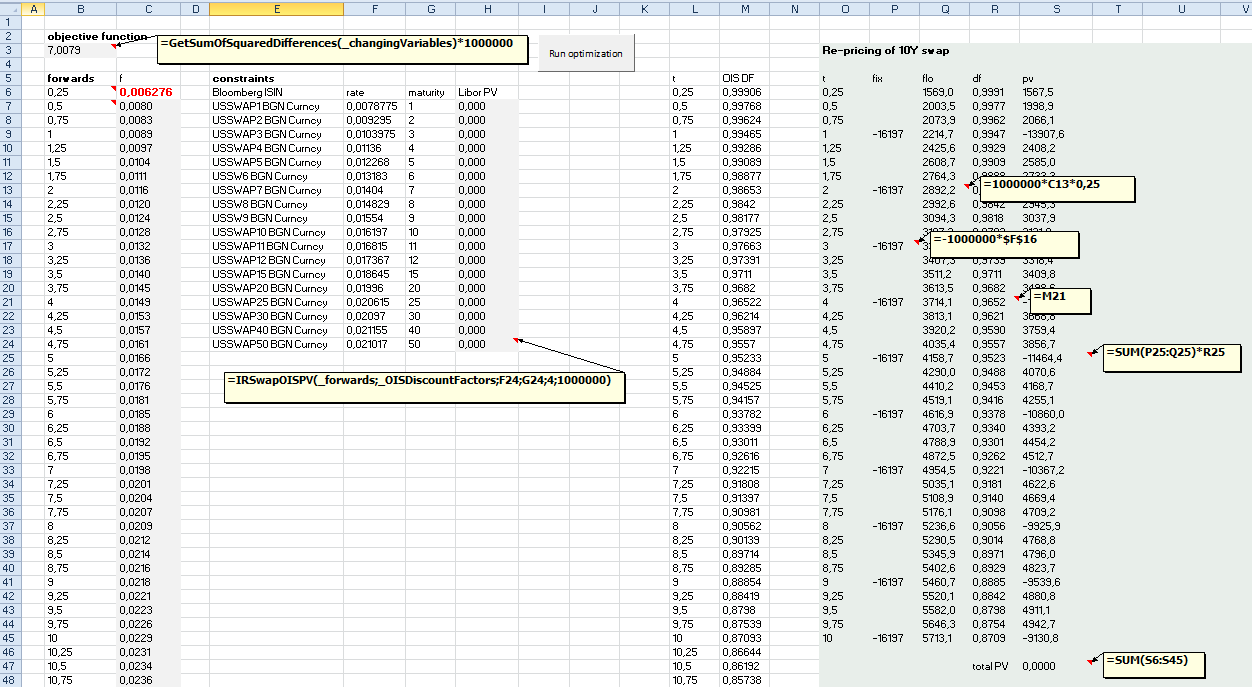

The results from this calibration model have been verified against the previous results.

Importing several files into project may involve considerable amount of cruel and unusual repetitive labour. For this specific reason, I have also been woodshedding a separate module (employing VBIDE object), which might give some relief when babysitting those AlgLib modules.

' The following dll libraries need to be referenced : ' Microsoft Visual Basic for Applications Extensibility 5.X, Microsoft Scripting Runtime Option Explicit Option Base 0 ' ' address to a list, which contains all BAS files which will be included into project Const listFolderPathName As String = "C:\AlgLib\vba\AlgLibLMAModules.txt" ' address to a folder, which contains all AlgLib BAS files Const moduleFolderPathName As String = "C:\AlgLib\vba\alglib-2.6.0.vb6\vb6\src\" ' select TRUE, if Require Variable Declaration in editor is tagged Const removeOptionExplicitDirective As Boolean = True ' Public Sub ImportModules() ' ' create a list of modules to be imported into this project Dim list() As String: list = createProjectModuleList ' import modules into active project import list End Sub ' Public Sub ExportModules() ' ' create a list of modules to be exported from this project Dim list() As String: list = createProjectModuleList ' export modules from active project into a defined folder export list End Sub ' Public Sub RemoveModules() ' ' create a list of modules to be removed from this project Dim list() As String: list = createProjectModuleList ' delete modules from active project remove list End Sub ' Private Function import(ByRef list() As String) ' Dim editor As VBIDE.VBProject Set editor = ActiveWorkbook.VBProject Dim fileSystem As Scripting.FileSystemObject: Set fileSystem = New Scripting.FileSystemObject ' ' loop through all files in a specific source folder for modules Dim filesInGivenList As Integer: filesInGivenList = UBound(list) + 1 If (filesInGivenList = 0) Then Exit Function ' Dim module As VBIDE.VBComponent Dim file As Scripting.file For Each file In fileSystem.GetFolder(moduleFolderPathName).Files ' ' if there is a given list of specific files to be included ' select only the files in that list to be imported into project If Not (moduleIsIncluded(file.Name, list)) Then GoTo skipPoint ' Set module = editor.VBComponents.Add(vbext_ct_StdModule) If (removeOptionExplicitDirective) Then module.CodeModule.DeleteLines 1 module.Name = VBA.Split(file.Name, ".")(0) module.CodeModule.AddFromFile file.Path skipPoint: Next End Function ' Private Function export(ByRef list() As String) ' Dim filesInGivenList As Integer: filesInGivenList = UBound(list) + 1 If (filesInGivenList = 0) Then Exit Function ' Dim editor As VBIDE.VBProject Set editor = ActiveWorkbook.VBProject Dim module As VBIDE.VBComponent ' ' loop through all modules For Each module In editor.VBComponents ' ' export module only if it is included in the list If (moduleIsIncluded(module.Name + ".bas", list)) Then module.export moduleFolderPathName + module.Name + ".bas" End If Next End Function ' Private Function remove(ByRef list() As String) ' Dim filesInGivenList As Integer: filesInGivenList = UBound(list) + 1 If (filesInGivenList = 0) Then Exit Function ' Dim editor As VBIDE.VBProject Set editor = ActiveWorkbook.VBProject Dim module As VBIDE.VBComponent ' ' loop through all modules For Each module In editor.VBComponents ' ' remove module only if it is included in the list If (moduleIsIncluded(module.Name + ".bas", list)) Then module.Collection.remove module End If Next End Function ' Private Function moduleIsIncluded(ByVal FileName As String, ByRef list() As String) As Boolean ' ' check if a given file name is in the list Dim isIncluded As Boolean: isIncluded = False Dim i As Integer For i = 0 To UBound(list) If (FileName = list(i)) Then isIncluded = True Exit For End If Next i moduleIsIncluded = isIncluded End Function ' Private Function createProjectModuleList() As String() ' ' create a list of file names from text file Dim fileSystem As Scripting.FileSystemObject: Set fileSystem = New Scripting.FileSystemObject Dim fileReader As Scripting.TextStream: Set fileReader = fileSystem.OpenTextFile(listFolderPathName, ForReading) Dim fileStreams As String: fileStreams = fileReader.ReadAll Dim streams As Variant: streams = VBA.Split(fileStreams, VBA.vbNewLine) Dim list() As String: ReDim list(0 To UBound(streams)) Dim i As Integer For i = 0 To UBound(streams) list(i) = VBA.Trim(streams(i)) Next i createProjectModuleList = list End Function '

Finally, thanks for reading this blog.

-Mike